powered by

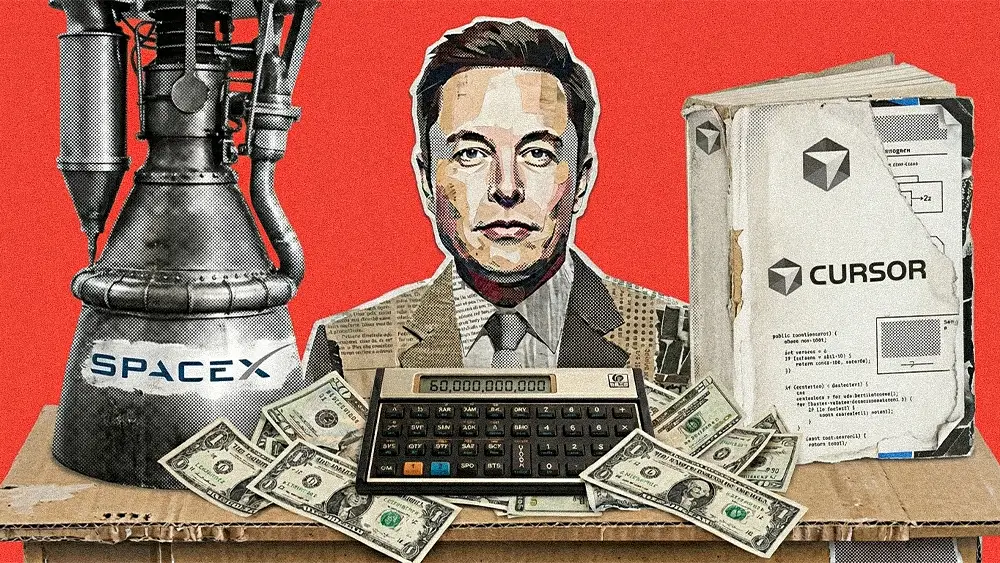

Last week SpaceX went public on the Nasdaq in the largest initial public offering ever recorded, raising north of $80 billion and crossing a $2 trillion valuation.

Last week SpaceX went public on the Nasdaq in the largest initial public offering ever recorded, raising north of $80 billion and crossing a $2 trillion valuation. Three trading days later it filed an 8-K agreeing to buy Anysphere, the company behind Cursor, in an all-stock deal that values the AI coding startup at $60 billion. The stock SpaceX is paying with did not exist as a tradable asset eight days earlier.

The market liked it. SpaceX shares rose roughly 16% on the day, leapfrogging Amazon and Microsoft by market value and lifting the company into the top tier of US public companies. Because the valuation is so high, the deal barely moves SpaceX's cap table. The $60 billion comes to about 3.4% dilution, a point Bill Ackman made on X within the hour: the more valuable SpaceX is, the cheaper its acquisitions get.

We covered the first chapter of this back in May, when SpaceX took its option on the company. The headline on that piece was that the deal said everything about where moats are now. Tuesday settled the question. It also surfaced something we had underweighted at the time. Being first to the public markets in this cycle does not only win you the story. It hands you the currency to act on the story while every rival is still private.

In April, SpaceX set up an unusual arrangement: it could either acquire Cursor for $60 billion later in the year or walk away and pay around $10 billion for the work the two companies had already done together. It waited to close until the IPO cleared, then exercised the option on Tuesday. The merger runs through a subsidiary, closes in the third quarter pending regulatory approval, and converts every Cursor share into SpaceX Class A stock at a price set by SpaceX's average close over the seven trading days before the deal goes through.

So the currency question answers itself. SpaceX printed acquisition-grade stock on the public markets and spent it before the IPO glow had faded. OpenAI and Anthropic, both building toward listings of their own, cannot do the same yet. That is not a marginal advantage in a market consolidating this quickly. It is the line between being the buyer and being a line on someone else's acquisition list.

Cursor is a real business, not a moonshot. Founded in 2022, it crossed $1 billion in annualized revenue last November and now sits at roughly $2.6 billion, almost all of it enterprise. Its Series D in November priced the company at $29.3 billion. By April it was reportedly raising fresh capital at around $50 billion, with Andreessen Horowitz, Nvidia, and Thrive Capital lined up. SpaceX's $60 billion clears every one of those marks.

The interesting part is the posture, not the price. Cursor was the holdout. It turned down two separate approaches from OpenAI. Microsoft looked at buying it and chose not to bid. Its leadership wanted to stay independent, and that independence was part of why developers trusted it in the first place. Cursor was the coding tool that did not belong to any of the model labs it ran on top of. That was the brand, and it was worth something specific.

There is a wrinkle in the fairy tale, though. Cursor's share of the AI coding market had been slipping before the sale, falling from about 41% in June 2025 to roughly 26% by May, with Anthropic taking close to half the category on the strength of Claude. The independent darling was being outrun on product at the exact moment it found a buyer willing to pay a premium for the independence it was about to give up.

SpaceX did not need Cursor's model. It absorbed xAI in February, folded it in as SpaceXAI, and already had Grok and the Colossus supercluster behind it. The two had spent months jointly training a model on that hardware, headed for both Cursor and Grok Build. The intelligence was never the scarce ingredient here.

What SpaceX bought was the surface. The enterprise revenue, the developer audience, the team, and a distribution channel into the one category where AI has reliably turned into business revenue, bolted onto a stack nobody else can assemble. Reusable rockets, the largest concentration of training compute on the planet, Starlink as an always-on network, energy, frontier models, and now an end-to-end software development engine sitting on top of all of it.

We have made this argument in three other places this year and it keeps holding. When Microsoft shipped a legal agent inside Word and made Harvey's $11 billion bet look a lot more fragile, the lesson was that a capability anyone can bundle into infrastructure they already own stops being a standalone business. When we wrote that AI was eating most of the execution layer of marketing and leaving only the strategic brand work behind, the lesson was the same. The thing that gets cheap is the doing. The thing that holds value is the judgment, the trust, and the system wrapped around it. SpaceX just applied that logic to code and put $60 billion behind it.

Not software. Code editors are replaceable and getting more so by the month. What Cursor sold was its neutrality, the reason a developer picked it over a tool owned by the lab whose model it was calling. That is a genuine brand asset, and it is also the first thing that gets repriced the moment the company becomes a SpaceX subsidiary sitting next to Grok.

This is the part no filing can resolve. SpaceX can buy the revenue and keep the team. Whether it can keep the trust that came from being unaffiliated is a separate question, and the answer will show up in churn numbers and developer sentiment long before it shows up in a press release. We have watched this gap open before. When Starbucks sold an AI rollout on a clean 99% accuracy figure and then quietly walked it back nine months later, the distance between the promise made in public and the reality underneath it was the whole story.

If you want a clean illustration of what we mean by The Great Flattening, read the announcement posts.

Cursor's new president of global revenue welcomed the deal with a LinkedIn post describing a "deep sense of mission" to build AI that would make the world more fraternal, drive engagement, and elevate the human experience, with lasting impact on society, the planet, and, in his words, the galaxy. There is an emoji on the end of it.

This is the biggest software acquisition of the year, and the words around it could have been generated by anyone for any deal in any sector. They carry no information about why these two companies belong together or what either one believes. We documented this pattern earlier in the year with hard data, the same handful of constructions spreading across corporate filings until every company sounded interchangeable. The post is a textbook case. A company has the most attention it will ever command, and it reaches for language so generic it disappears.

When the product underneath you commoditizes, value migrates to two places: the stack you own and the story only you can tell. SpaceX is betting almost everything on the stack, and it is the hardest position in the market to copy. If your company's advantage is a single capability a larger platform could fold into something it already sells, you are closer to Cursor than you want to be, and you should be planning for it now rather than after the option gets exercised.

The story half is just as real, and it is the one most companies fumble. Independence and trust sit on the balance sheet whether or not anyone accounts for them, and they are fragile in exactly the moments that look like wins. Cursor's neutrality meant something concrete to the developers who chose it. None of that transfers cleanly to a subsidiary of the company building Grok. Whether SpaceX can hold what it paid for is the open question, and no amount of stock answers it.

One more thing, because it is the cheapest mistake on this list to avoid. Your loudest moment is your most exposed one. When the whole market is watching, generic language is not a safe default, it is a risk you are choosing to take. The companies that come out of this phase ahead will be the ones whose voice is distinct enough to survive their own announcements.

SpaceX won the race, banked the currency, and spent it inside a week. The deal was the easy part. The harder test is whether the trust and the independence it just bought still mean anything once they belong to the largest company on the launch pad. We will be reading what they publish next, and listening for whether it sounds like anyone at all.

The best editorial systems don’t happen by accident. Outlever builds them.

The best editorial systems don’t happen by accident. Outlever builds them.

Subscribe for the kind of thinking that makes people stop, read and come back.